Media Futures is an annual benchmarking project, now in its ninth year, undertaken by Wessenden Marketing in partnership with InPublishing.

The results of the latest 2018 survey involving 83 media companies have just been released. So, what is the latest take on the media business?

Media Futures 2018 is showing that while publishers are finding it tough going this year, things are better than in 2017 and that there is more optimism about 2019. The four key industry metrics provide more detail.

1. Turnover Growth

65% of the participating companies report that their top-line turnover is currently growing, coming back up after a big dip in 2017. The industry is even more bullish about next year with the figures rising again. Currently, turnover growth among the benchmarking companies is averaging out at +5%, up from +3% last year, with a prediction that the rate will accelerate to +6% next year.

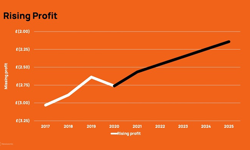

2. Profitability

80% of the participating companies are currently in profit. As with turnover, this a better figure than in 2017 and is forecast to rise again next year. Looking at the actual profit margins of those companies that are in the black, these are averaging 9% now with 11% predicted for next year. Despite all the pressures, the media business is still delivering profit margins that many other industries would kill for. Yet this is the result of ongoing and grinding cost control which is now baked into the culture of most companies.

3. Headcount

The headcount metric is the one that dived most dramatically in 2017 – clearly a year when major staff culls took place. With turnover growing faster than headcount, the industry’s productivity figures are increasing, but many companies are finding the pressures intense. A common theme running through the survey is that there are simply not enough people resources to get through the “to do” list, which continues to grow longer and longer at the same time as the delivery deadlines get shorter and shorter.

4. Marketing Budgets

The marketing budget metric is the only one that is down year-on-year: 42% of companies are stating that their spend on advertising and promotion, customer research, etc is increasing. This figure is down from 48% last year. Not only is the industry’s spend falling, but that spend is being spread more thinly across an increasing range of areas. It is also clear that it is development areas, typically digital, which are drawing money out of more established, legacy activities – the print newsstand being a prime example for many consumer publishers.

So, all the figures underline the fact that 2018 is looking to be slightly better than last year, but that things are still very tough. Tight cost control is running in parallel with modest investment. That investment has shifted slightly away from brands and marketing and into people. At the same time, confidence levels about the future success of the company are edging up after last year’s dive, but they are still well below those of previous years and there is a real sense that there is massive, rapid and accelerating change around the corner. So, there is still considerable nervousness about the year ahead.

Behind these top-line figures, there also some subtle, but real shifts in emphasis in Media Futures 2018:

* Moving to “audience first”. The focus on platform which has characterised past surveys (the drive to be “digital first” or “mobile first”) is clearly morphing into a more pragmatic “audience first” approach, where the end user determines what the platforms are. There is a lot of evidence, mainly in consumer media, to show that there are still many “print first” companies currently running strong and profitable businesses with minimal digital revenues. Yet long-term, that may well be a very dangerous place to be.

* Moving from cost-cutting to revenue building, where there is now more focus on driving top-line sales. That is linked to two other factors. Firstly, the need to diversify the revenue streams, which is balanced by a justifiable concern about doing too many things at the same time. The key diversification areas are ecommerce, live events, content marketing and international expansion. Secondly, there is a clear shift in emphasis from doing lots of shiny new things to doing existing things better.

* Moving from “energy” to “experience”. The blind dash to bring in raw young talent with new ideas, digital savvy and disruptive approaches to working is now being tempered by a growing appreciation of knowledge, experience and consistency.

So, there are no silver bullets and no business models that guarantee success in every market; just a dizzying mix of challenges and opportunities, where there are four key requirements:

* Insight into both the audiences served and how one’s own organisation actually works.

* Balancing conflicting factors: top-line growth versus bottom-line profitability: what works now versus what might work in the future; energy versus experience; DIY versus partnerships and cooperation; creative disruption versus mindless chaos.

* Productivity: AI in all its manifestations and applications must drive increased productivity in every area of activity.

* Ruthless prioritisation as there are simply too many things on the “to do list” to execute them all well.

In coming articles, we shall look at what that all means in practice.